A good credit score is key for your financial health. It affects loan approvals, interest rates, and even getting an apartment. Improving your score might seem hard, but it’s doable with the right steps.

Boosting your credit score by 100 points in 2 months is tough. But, with a clear plan, it’s possible. Knowing what impacts your score and taking action can help you improve your credit score fast.

With a better credit score, you’ll unlock more financial doors. You’ll get lower interest rates on loans and credit cards. This section will guide you on how to boost your credit score improvement significantly.

Key Takeaways

- Understand the factors that affect your credit score.

- Learn strategies to improve your credit score quickly.

- Discover how to maintain a good credit score over time.

- Explore the benefits of having a high credit score.

- Find out how to check your credit report and score.

Understanding Credit Score Fundamentals

Knowing the basics of credit scores is key for better financial health. Your credit score is a three-digit number. It shows how trustworthy you are to lenders.

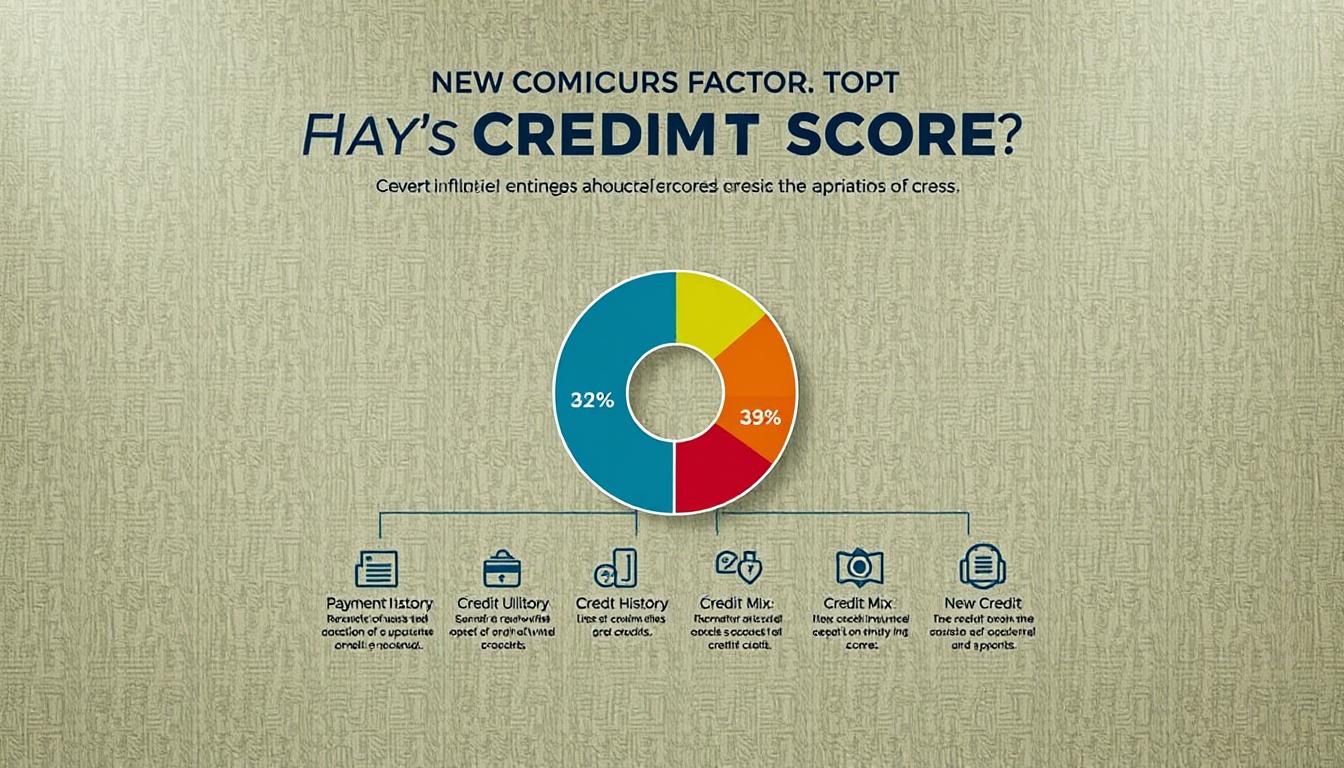

The Five Factors That Determine Your Score

Your score is based on five main factors. These are payment history, credit utilization, length of credit history, credit mix, and new credit inquiries. Payment history counts for 35% of your score. Knowing these credit score factors helps improve your score.

Why a 100-Point Jump Changes Your Financial Options

A 100-point score boost opens up better financial options. It can mean better loan terms, lower interest rates, and higher credit limits. This credit score impact can save you money and give you more financial freedom.

Setting Realistic Timeframes for Improvement

Improving your credit score takes time. It’s important to have realistic goals. Quick improvements are possible, but big changes take months to years. Knowing the credit score impact of your actions helps set reachable goals.

Quick-Impact Actions for Two-Month Results

In just two months, you can boost your credit score a lot. To see a 100-point jump, focus on actions that directly affect your credit score.

Requesting Strategic Credit Limit Increases

One smart move is to ask for a credit limit increase on your cards. This can help your credit utilization ratio, a key score factor. Here’s how:

- Look for cards with high limits and low balances.

- Call your issuer to ask for a limit hike.

- Be ready to share your financial details to back your request.

Having a higher limit makes it simpler to keep your credit utilization low. This is good for your score.

Leveraging Authorized User Status on Established Accounts

Being an authorized user on someone else’s account is another quick fix. It’s great if the main account holder has a long history and low usage.

Key considerations:

- Make sure the account is in good shape.

- Check if the account info is shared with credit bureaus.

- This method might not work if the main account has bad credit.

When to Consider Rapid Rescoring Services

Rapid rescoring services are good if you’ve made big changes to your credit and need a fast score update. They’re especially helpful for those applying for mortgages.

It’s crucial to think about the costs and benefits of rapid rescoring. It’s not for everyone.

Strategic Payment Planning for Maximum Impact

Strategic payment planning is key to boosting your credit score. By managing your payments wisely, you can see big improvements quickly.

Prioritizing Past-Due Accounts by Age and Impact

When tackling past-due accounts, focus on the oldest ones first. They hurt your score more, so fixing them quickly helps more.

| Account Age | Impact on Credit Score | Priority Level |

|---|---|---|

| Over 2 years | High | High Priority |

| 1-2 years | Moderate | Medium Priority |

| Less than 1 year | Low | Low Priority |

Creating a 60-Day Payment Calendar

A 60-day payment calendar keeps you on schedule. It shows creditors you’re reliable with payments, boosting your score.

Scripts for Negotiating with Creditors

Talking to creditors can be tough, but scripts help. For instance, say, “I understand I missed a payment, and I’m ready to fix it. Can we talk about a payment plan or settlement?”

These scripts help you talk clearly. They might lower what you owe or set up a doable payment plan.

Optimizing Credit Utilization Ratios

Improving your credit score starts with managing your credit utilization ratio. This is a key factor in how your credit score is calculated.

The credit utilization ratio shows how much of your available credit you’re using. Keeping this ratio low is crucial for a good credit score. Aim for a utilization ratio between 10% and 30% for all your credit cards.

Achieving the Ideal 10-30% Utilization Range

To hit the ideal range, balance your credit card balances. Using less than 30% of your credit shows lenders you handle it well.

- Calculate your total available credit and current balances.

- Adjust your spending habits to maintain a low utilization ratio.

- Consider increasing your credit limit to lower your utilization ratio.

Strategic Card Balance Distribution Techniques

Spreading your credit card balances can help your credit score. Spread your balances across multiple cards instead of maxing one out.

| Card Name | Credit Limit | Current Balance | Utilization Ratio |

|---|---|---|---|

| Card A | $1000 | $200 | 20% |

| Card B | $2000 | $300 | 15% |

Mid-Cycle Payment Timing for Reporting Benefits

Strategic payment timing can also boost your credit score. Paying before the statement cycle ends can lower your reported balance. This improves your utilization ratio.

“The key to a good credit score is not just about having credit, but about managing it wisely.”

Effective credit management requires constant monitoring and planning. By aiming for the right utilization range, spreading balances, and timing payments, you can greatly enhance your credit score.

How to Boost Your Credit Score 100 Points in 2 Months

To boost your credit score by 100 points in two months, you need a solid plan. This section will guide you through a detailed, week-by-week strategy to help you reach your goal.

Week 1-2: Assessment and Quick Wins

The first two weeks are key for checking your credit and getting quick wins.

- Get a copy of your credit report from all three major credit bureaus.

- Dispute any errors or inaccuracies found.

- Make timely payments to avoid late fees.

Week 3-6: Strategic Debt Reduction

Weeks 3-6 are for reducing debt smartly.

- Prioritize debts with the highest interest rates or the smallest balances.

- Consider consolidating debt into a lower-interest loan or credit card.

Week 7-8: Fine-Tuning and Final Push

The last two weeks are for fine-tuning your credit and a final push.

- Review your credit utilization ratio and adjust as necessary.

- Avoid applying for new credit to prevent temporary score reductions.

By sticking to this 8-week plan, you can greatly improve your credit score. Key steps include checking your credit report, reducing debt, and adjusting your credit utilization.

Addressing Negative Items on Your Report

Improving your credit score can be tough, especially with negative report items. Things like late payments, collections, or bankruptcies can really hurt your score. But, there are ways to tackle these problems.

Step-by-Step Dispute Process for Errors

Disputing errors on your credit report is key to bettering your score. First, find the mistake, then collect proof, and finally, send a dispute to the credit agency.

- Get a copy of your credit report from the three major agencies.

- Check the reports for any mistakes or wrong information.

- Collect documents that back up your dispute, like payment records or letters from creditors.

Writing Effective Goodwill Letters for Removal

A goodwill letter asks a creditor to remove a negative mark from your report. It works best if you explain the reason for the mark and show you’ve been paying on time.

Key elements of a goodwill letter:

| Element | Description |

|---|---|

| Acknowledgment | Admit the negative mark and take responsibility. |

| Explanation | Give a valid reason for the mark. |

| Positive History | Show your good payment history with the creditor. |

Pay-for-Delete Negotiations with Collection Agencies

Pay-for-delete deals mean paying a collection agency to remove the mark from your report. It’s a good way to boost your score, but you need to negotiate well.

Tips for successful pay-for-delete negotiations:

- Make sure you know the exact debt amount and details.

- Offer a fair price based on the debt and your finances.

- Get the agreement in writing before paying anything.

Monitoring and Tracking Your Progress

Improving your credit score means keeping an eye on your progress. Tracking your score regularly shows how your actions affect it. This helps you make better choices.

Free vs. Paid Credit Monitoring Services

Credit monitoring services come in two types: free and paid. Free services give you basic features like score tracking and alerts for big changes. Paid services offer more, like detailed credit reports and protection against identity theft.

“Experian’s credit monitoring service provides identity theft protection and up to $1 million in insurance coverage.”

Understanding Score Fluctuations During Improvement

Your credit score can change for many reasons, like how much you use credit and your payment history. It’s important to understand these changes to manage your score well. For example, one late payment can drop your score a lot, but paying on time can raise it.

Using Score Simulators to Predict Results

Score simulators help guess how your financial moves will change your credit score. They let you see what might happen if you apply for new credit or pay off debt.

Using these tools and knowing how scores change can help you make smarter financial choices. This way, you can reach your financial goals more easily.

Conclusion: Maintaining Your Improved Score

Boosting your credit score by 100 points in two months is a big win. But keeping that score up is just as crucial for your long-term financial health. To keep your score high, keep making payments on time and use your credit wisely.

It’s also key to watch your credit report and score closely. This way, you can catch any problems early. You might want to use free or paid services to keep an eye on your credit and get alerts about any changes.

Having a good credit score can help you reach your financial dreams. It can make getting a mortgage or a car loan easier. It can even help you get better interest rates on your credit cards. Stay on track with your credit management plan to enjoy the perks of a strong credit score for years to come.

FAQ

What factors determine my credit score?

Your credit score is based on several things. These include your payment history, how much credit you use, and how long you’ve had credit. It also looks at your credit mix and recent credit inquiries.

How can I improve my credit utilization ratio?

To better your credit utilization, keep your card balances low. Aim for 10% to 30% of your credit limit. Also, spreading your debt across different cards can help.

What is the ideal credit utilization range?

The best range for credit utilization is 10% to 30%. Staying below 30% shows you can handle your debt well.

How do I dispute errors on my credit report?

First, get a copy of your credit report. Then, find the errors and dispute them with the credit agency. Make sure to include proof of your claim.

Can becoming an authorized user on someone else’s account help my credit score?

Yes, being an authorized user can boost your score. It works if the main account holder has good credit and pays on time.

What is rapid rescoring, and how does it work?

Rapid rescoring quickly updates your credit report. It can reflect paid debts or corrected errors. This can improve your score in a few days.

How often should I check my credit report?

Check your credit report at least once a year. Do it more often if you’re trying to improve your score.

What are score simulators, and how can they help me?

Score simulators predict how your financial actions will affect your score. They help you make smart choices.

How long does it take to see improvements in my credit score?

Seeing score improvements takes time, depending on your situation. But with steady effort, you can see changes in a few months.

What is a goodwill letter, and how do I write one?

A goodwill letter asks a creditor to remove a negative mark. To write one, explain the situation and show you’ve managed your credit well since then.